Social Security’s 2032 Crisis: The Bipartisan Solution That Can Prevent Benefit Cuts

Social Security is not on the brink of collapse. However, a significant threat of benefit reductions in the 2032-33 timeframe looms due to projections that the primary trust fund will deplete its reserves during that period.

The program operates as a “pay-as-you-go” system, meaning current workers fund current retirees’ benefits. For decades, Social Security collected more revenue than necessary for payouts, accumulating over $2.9 trillion in the OASDI Trust Fund by 2021. Since then, the growing number of baby boomers receiving benefits has created a shortfall, causing rapid depletion of the trust fund to cover current obligations.

Without intervention, retirees could face a 23% reduction in benefits when the fund runs dry. For millions who depend on Social Security as their primary income source, such cuts would severely impact housing, healthcare, and essential living expenses.

The pay-as-you-go model originated during the Great Depression to provide immediate support to older Americans without savings or pensions. Instead of building a large investment fund, payroll taxes were distributed directly, creating an intergenerational financial compact. Over time, demographic shifts—including increased life expectancy and declining birth rates—have strained this structure while the fundamental framework remains intact.

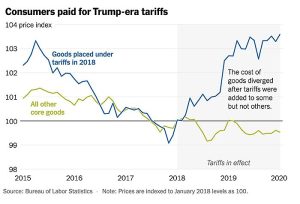

To restore solvency, one proposed solution involves redirecting tariff revenue to Social Security. Tariffs generate substantial federal revenue when applied broadly, potentially closing the funding gap without raising payroll taxes or reducing benefits. However, tariffs also raise consumer prices, disproportionately affecting retirees on fixed incomes. Current estimates suggest such tariffs could cost families up to $1,200 annually.

In contrast, a 23% benefit reduction would cost the average retired couple approximately $18,100 per year. Therefore, using tariff revenue to bolster Social Security would yield far greater benefits for over 70 million Americans than any associated costs.

Another option is covering shortfalls through borrowing from the general fund. But this approach undermines the pay-as-you-go principle and increases national debt by shifting burdens to future generations rather than maintaining intergenerational balance.

A more historically effective solution, demonstrated during President Reagan’s administration in the early 1980s, was establishing a bipartisan commission. The Greenspan Commission extended Social Security’s solvency by over 50 years through consensus-based recommendations. Today, with the 2032 deadline approaching, Americans should urge their representatives to encourage President Trump to appoint a new Reagan-style commission to address Social Security’s long-term stability.